Enforcement of Corporate Reporting

Corporate reporting enforcement across the EEA is anchored in a unified supervisory architecture that promotes transparent, high quality disclosures for investors.

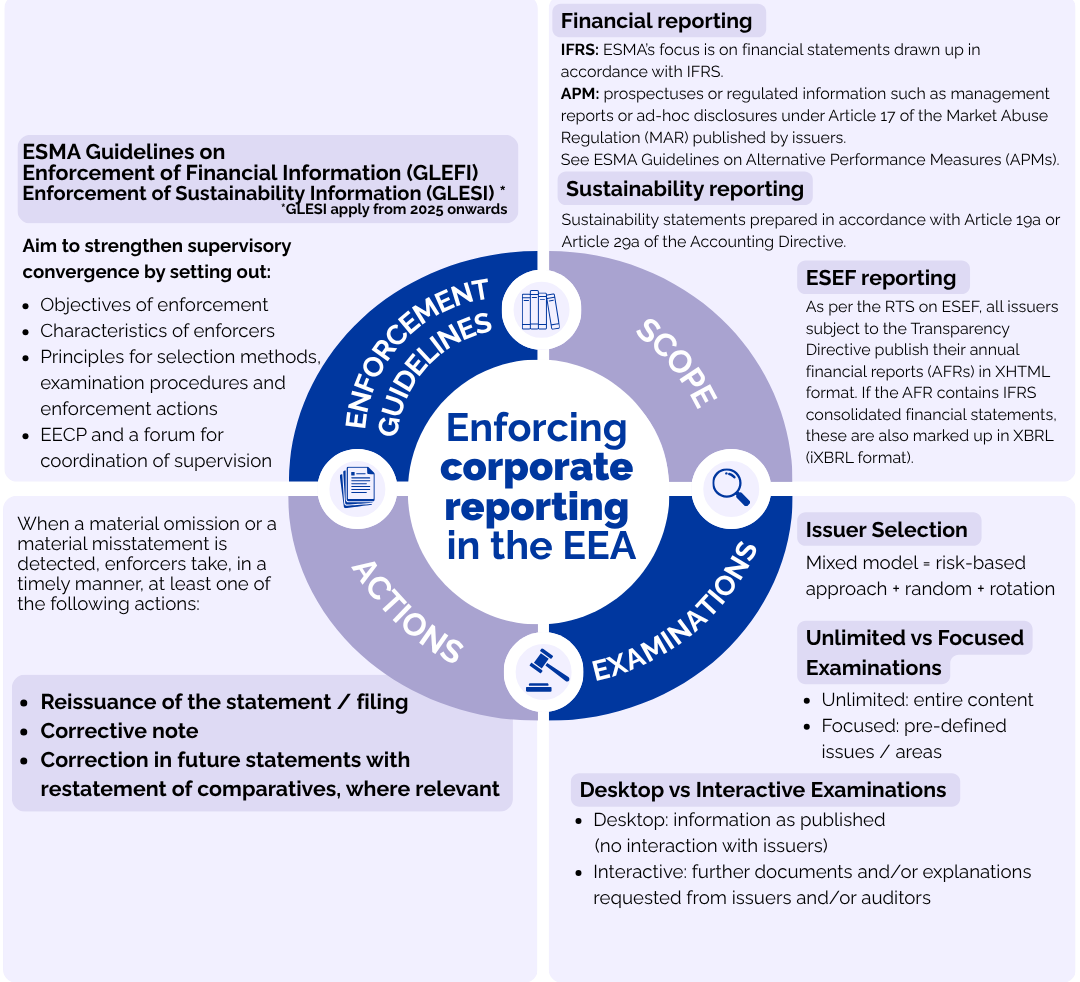

Enforcement of corporate reporting in the EEA operates within a coherent and harmonised supervisory architecture designed to safeguard the quality and transparency of information available to investors and the wider market. Building on ESMA’s long‑standing efforts to promote convergence, this framework brings together common principles, coordinated methodologies and shared European Common Enforcement Priorities (ECEP) across EEA jurisdictions. This section explains how this system functions in practice across financial reporting, sustainability reporting and European Single Electronic Format (ESEF) reporting, highlighting both the underlying principles and the practical tools that support consistent enforcement throughout the EEA.

To help visualise the outcome of the enforcement process and what activities ESMA and enforcers carry out in practice, ESMA publishes each year a comprehensive Report on Corporate Reporting Enforcement and Regulatory Activities, which not only presents detailed descriptive enforcement statistics but also offers rich technical insights, assessments against the ECEP and a consolidated overview of key publications and supervisory messages issued throughout the year.

Annual Report on corporate reporting enforcement and regulatory activities

Financial Reporting

How IFRS reporting is enforced

Background

In 2014, ESMA published its Guidelines on Enforcement of Financial Information (the Guidelines/GLEFI), aimed at strengthening supervisory convergence in the enforcement practices amongst the national competent authorities (NCA) designated in each EEA country. In 2022, a revised version of the Guidelines became effective.

Enforcers are required to confirm in writing to ESMA whether they comply, intend to comply, or do not (intend to) comply with the Guidelines. Currently, 26 of 30 EEA countries have indicated to ESMA that they comply with the revised version of the Guidelines, while one NCA has declared that it intends to comply in the near future.

Focus

The Guidelines define the objectives of enforcement, the characteristics of enforcers and set out the principles to be followed throughout the enforcement process, such as selection methods, examination procedures and enforcement actions. They also strengthen the convergence of enforcement activities at European level by introducing the ECEP and providing enforcers with a forum to coordinate their views on accounting matters prior to taking enforcement decisions at national level, the Financial Reporting Working Group (EECS) (FRWG (EECS)).

Financial information of issuers is subject to enforcement, regardless of which reporting framework has been applied. Although the focus for ESMA is on financial information drawn up in accordance with IFRS as endorsed by the EU (for consolidated and non-consolidated financial statements), enforcers also examine financial information prepared in accordance with:

- National Generally Accepted Accounting Principles (GAAP) (for non-consolidated financial statements),

- IFRS as issued by the IASB

- Third country accounting standards, if those are deemed equivalent to IFRS as endorsed in the EU (for financial statements of non-European issuers).

Key definitions and concepts

“Enforcement” refers to examining compliance of financial information with the applicable financial reporting framework as well as taking appropriate measures when infringements are identified.

Enforcers identify the most effective way for enforcement of financial information. Each enforcer’s selection of issuers for examination is based on a mixed model whereby a risk-based approach is combined with random sampling and rotation. A risk-based approach considers the risk of a misstatement as well as the impact of a misstatement on the financial markets. Enforcers can use either unlimited scope examinations or a combination of unlimited scope and focused examinations of financial information of issuers selected for enforcement. Depending on the enforcer’s interaction with issuers, examinations are classified as interactive or desktop examinations.

An unlimited scope examination entails the evaluation of the entire content of the financial information to identify issues or areas which require further analysis, while a focused examination refers to the evaluation of pre-defined issues / areas in the financial information. Both entail an assessment of whether this information is compliant with the relevant financial reporting framework. However, the depth and scope of an examination as prescribed in GLEFI cannot be equated with those of an audit of financial statements.

According to Guideline 7, when a material misstatement is detected, enforcers should, in a timely manner, take at least one of the following actions:

- Require a reissuance of the financial statements: This action leads the issuer to publish revised financial statements which may be subject to a new audit opinion,

- Require a corrective note: This action entails that either the issuer or the enforcer itself publishes a note in relation to a material misstatement with respect to the particular item(s) included in already published financial information generally together with the corrected information (unless impracticable), or

- Require correction in future financial statements with restatement of comparatives, where relevant: When an enforcer takes this action, the issuer either adopts an acceptable treatment in the next financial statements and, where relevant, corrects the prior year by restating the comparative amounts or includes additional disclosures which may not require the restatement of comparatives.

The assessment of whether a departure from the standards is material is made in accordance with the relevant financial reporting framework. In relation to financial reports prepared in accordance with IFRS, paragraph 7 of IAS 1 Presentation of Financial Statements states that information is considered material if omitting, misstating, or obscuring it could reasonably be expected to influence decisions that the primary users of financial statements make on the basis of those financial statements.

Depending on the nature of the items to which the identified departure from the standards relates, enforcers consider quantitative and/or qualitative factors to determine whether a departure could reasonably be expected to influence the decisions of users. As the assessment of materiality of disclosures involves qualitative considerations to a greater extent, for enforcers it is key that the disclosures provided in financial statements are informative, comprehensive and clear to enable an understanding of the transactions or events having occurred in a given year and how the principles of recognition, measurement and presentation have been applied by issuers.

The assessment of materiality often requires judgement and depends on entity-specific facts and circumstances. Therefore, the decision regarding which specific quantitative thresholds and qualitative criteria are to be applied in the context of an individual issuer's financial statements is made by the enforcer conducting the examination of those financial statements.

The IFRS Practice Statement 2 Making Materiality Judgements published by the International Accounting Standards Board (IASB) in 2017, which includes an overview of the general characteristics of materiality and presents a four-step materiality assessment process, provides helpful guidance on how to make materiality judgements in specific circumstances.

When deciding which type of action to apply, enforcers should consider (subject to the existing powers of the enforcer) that the final objective is that investors are provided with the best possible information. Therefore, an assessment should be made as to whether the original financial statements and a corrective note provide users with sufficient clarity for taking decisions or whether a reissuance of the financial statements is more appropriate. Other factors should also be considered, namely timing, the nature of the decision and the surrounding circumstances. For instance, a correction in future financial statements might be appropriate when (i) the decision is very close to the date of the publication of the next financial statements (which could also be the interim financial statements of the issuer), (ii) the market is sufficiently informed at the moment the decision is taken or (iii) the decision relates merely to the way information was presented in the financial statements rather than to the substance (e.g., material information is clearly presented in the notes or elsewhere in the financial report, for instance in the management report, whereas the relevant accounting framework requires the presentation on the face of the primary financial statements or in the notes).

Furthermore, enforcers seek to improve the quality of future financial statements by engaging in activities designed to provide helpful guidance to issuers, such as defining enforcement priorities and / or a pre-clearance procedure. Even when no enforcement actions are required, enforcers often make recommendations during the examination process on how certain disclosures could be improved by issuers.

How APM reporting is enforced

ESMA Guidelines on Alternative Performance Measures (APMs)

ESMA’s Guidelines on APMs were published on the basis of Article 16 of the ESMA Regulation and became effective in 2016. The Guidelines on APMs set out principles for the presentation and disclosure of performance measures outside financial statements, such as labels, reconciliations, and definitions, to ensure that issuers comply with the “true and fair view” principle when publishing APMs.

The Guidelines on APMs are addressed to issuers whose securities are admitted to trading on a regulated market and who are required to publish regulated information as defined by the Transparency Directive, as well as to persons responsible for the prospectus under Article 11(1) of the Prospectus Regulation. They are aimed at promoting the usefulness and transparency of APMs included in prospectuses or regulated information such as management reports or ad-hoc disclosures published to market pursuant Article 17 of MAR. Adherence to the Guidelines improves the comparability, reliability, and/or comprehensibility of APMs. Issuers or persons responsible for the prospectus who comply with these Guidelines provide a true and fair view of the APMs disclosed in a prospectus.

ESMA has published several questions and answers on the Guidelines on APMs to promote common supervisory approaches and practices in their implementation (retrievable in the Q&A tool).

Sustainability Reporting

How sustainability reporting is enforced

ESMA finalised its Guidelines on the Enforcement of Sustainability Information (GLESI) in July 2024. The GLESI are closely modelled on the Guidelines on Enforcement of Financial Information (GLEFI) to ensure a comparable supervision of issuers’ sustainability and financial reporting, and as such, the GLESI envisage a principles-based approach to supervision and enforcement. Furthermore, the focus, key definitions and concepts of the GLESI are largely similar to those of the GLEFI, except where sustainability-related specificities apply.

The GLESI started applying to the enforcement of sustainability information published from 1 January 2025. As reflected in the GLESI compliance table, which is reviewed on an annual basis, the largest group of enforcers has informed ESMA that they comply with the GLESI, a smaller group has informed ESMA that they intend to comply with the GLESI by a given point in time (many of which due to the pending transposition of the Corporate Sustainability Reporting Directive (CSRD) in their Member State) and a residual group has informed ESMA that they do not comply with all parts of the GLESI at this stage.

In February 2025, the European Commission issued its Omnibus 1 legislative package to reduce the administrative burden for companies and increase competitiveness. This led to the publication of the Omnibus 1 Directive in the Official Journal of the European Union on 26 February 2026, reducing the scope of companies that have to report under the CSRD. As part of the Omnibus package, a process was also set in motion to revise the European Sustainability Reporting Standards (ESRS).

To acknowledge the uncertainty caused by the concurrent publication of the Omnibus proposals, the uneven transposition of the CSRD across Member States and the first reporting and supervision under the ESRS, ESMA published a statement in June 2025 which confirms enforcers’ continued commitment to transparent sustainability reporting and sets out their intention to pursue proportionate and realistic enforcement of sustainability reporting in this context. This statement remains a reference point for enforcers in 2026 as they undertake enforcement of financial year 2025 reporting.

Moreover, in consideration of the evolving regulatory context, ESMA carried over to its European Common Enforcement Priorities (ECEP) 2025 two of the priorities from ECEP 2024 (materiality, and scope and structure of the sustainability statements) which relate to fundamental features of sustainability reporting.

ESEF Reporting

How ESEF reporting is enforced

The Transparency Directive mandated ESMA to develop regulatory technical standards (RTS) on the European Single Electronic Format (ESEF). The RTS on ESEF requires all issuers subject to the requirements contained in the Transparency Directive to make public their annual financial reports (AFRs) in the Extensible Hypertext Markup Language (XHTML) format. Where issuers prepare IFRS consolidated financial statements, they shall mark up these IFRS consolidated financial statements using the XBRL markup language. The markups are embedded in the XHTML document version of the AFR using the Inline XBRL (iXBRL) format.

The ESEF requirements (XHTML and XBRL) started to apply to financial years beginning on or after 1 January 2020 for primary financial statements where all numbers in a declared currency need to be marked up (detailed tagging) and on or after 1 January 2022 for applying markups to larger pieces of information (block tagging) of the notes to the financial statements.

Enforcement of the requirements laid out in the RTS on ESEF follows the same principles that currently underpin the enforcement of financial reporting, mirroring its approach to issuer selection, examination procedures and the types of actions available to enforcers. Enforcement encompasses both automated validations and manual examinations. In practice, enforcers evaluate technical compliance through filing examinations, ensuring (among others) that the XHTML package is valid, the iXBRL architecture is sound and the correct taxonomy version has been applied. They also undertake markup examinations, assessing, among other topics, whether issuers have selected appropriate IFRS taxonomy elements, correctly anchored any extension taxonomy elements, ensured the completeness of mark‑ups and avoided inconsistencies between marked up values and the figures reported. Together, these layers of review drive the overall data quality of ESEF filings across the EEA, while also shaping the enforcement priorities (ECEP) for the next annual cycle.